A quality foot massager for diabetic neuropathy can cost anywhere from $80 to $300. That’s a real barrier for many people managing a chronic condition that’s already expensive to treat.

Here’s what most people don’t know: the right foot massager — bought the right way — can be purchased entirely with pre-tax FSA or HSA dollars. For someone in a 25% tax bracket, that’s effectively a 25% discount. For a $200 device, that’s $50 back in your pocket.

The catch is that not every foot massager qualifies. The rules depend on the device type, how it’s classified, and in some cases, whether your doctor has documented a medical need. This guide walks through all of it — clearly, without jargon.

If you are still comparing device types, start with our full guide to the best foot massager for neuropathy and diabetes, then use this article to understand the FSA/HSA payment rules.

| Quick Answer Many TENS units and medically classified electrical stimulation devices can be FSA or HSA eligible when used for pain relief or another qualified medical purpose. TENS machines are commonly listed as eligible medical devices, while standard shiatsu or relaxation-style foot massagers are usually conditional and may require a Letter of Medical Necessity from a healthcare provider.[1][2] For neuropathy, the safest approach is simple: choose a device with a clear medical purpose, keep an itemized receipt, and get a Letter of Medical Necessity if the product is a shiatsu, compression, or general massage device. Your own FSA/HSA plan administrator has the final say. |

FSA vs HSA: What’s the Difference and Which One Do You Have?

Before getting into which devices qualify, it helps to understand the account you’re spending from — because the rules differ slightly between FSA and HSA, and confusing them can cost you money.

| Feature | FSA | HSA |

|---|---|---|

| Full name | Flexible Spending Account | Health Savings Account |

| Who can have it? | Usually offered through an employer. | Available only with a qualified high-deductible health plan. |

| Rollover rules | Often use-it-or-lose-it, depending on your employer’s plan. | Rolls over indefinitely and belongs to you. |

| Best strategy | Use eligible funds before the plan deadline. | Spend now or save for future medical expenses. |

| Foot massager rule | Eligible when the product meets medical-expense rules or documentation requirements. | Same qualified medical-expense standard, but you control the account. |

Important: FSA rules vary by employer plan. HSA funds roll over, but non-qualified HSA spending can trigger income tax plus an additional 20% tax before age 65.

Contribution limits can change each tax year. Check IRS Publication 969 or your plan administrator for the latest HSA limits, and check your employer plan documents for your FSA annual limit.[3]

| The most important FSA rule for diabetics: FSA funds typically expire on December 31 each year. If you have unspent FSA dollars approaching year-end, buying a qualifying therapeutic foot massager is one of the smartest ways to use them before they disappear. HSA funds never expire — you can save them indefinitely [4]. |

The IRS Rule: What Makes a Foot Massager a Medical Expense?

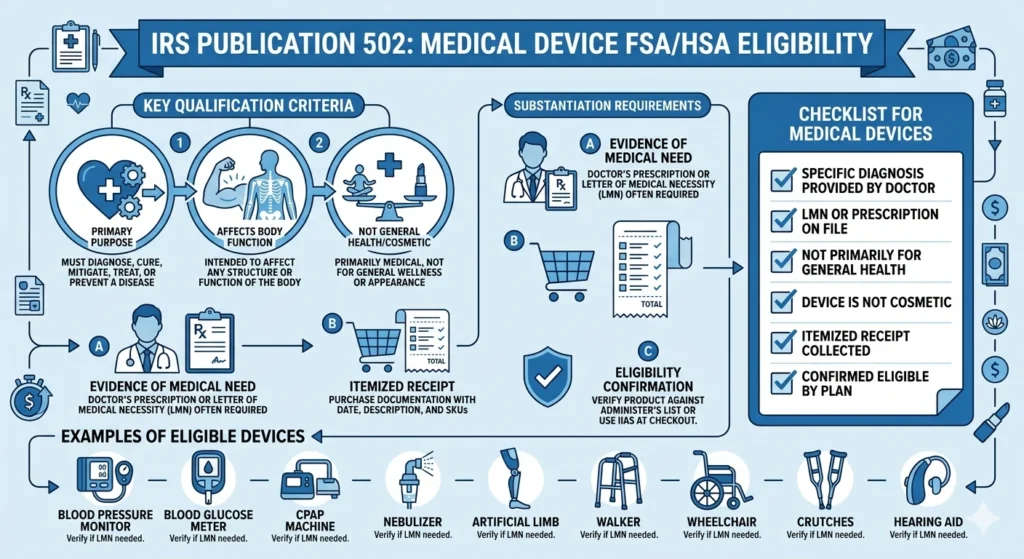

The IRS definition of a qualified medical expense comes from IRC 213(d)(1), which states: medical care includes amounts paid for the “diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body.” This explicitly includes medical equipment, supplies, and diagnostic devices needed for these purposes.[1].

The critical test is called the primary purpose test. For a product to qualify, its primary purpose must be medical — not general wellness or relaxation. A foot massager bought because your feet are tired after work fails the test. The exact same device bought as part of a documented treatment plan for diabetic neuropathy can pass it.

That distinction is everything. The device itself doesn’t change — the documented medical purpose does.

Why TENS and EMS Devices Are Treated Differently From Shiatsu Massagers

TENS units have a clear medical classification. The FDA categorises them as Class II medical devices, and their specific therapeutic function — electrical nerve stimulation for pain management — places them squarely within the IRS’s definition of a medical device.

FSAstore lists TENS machines as eligible for reimbursement with an FSA, HSA, or HRA.[2]

Shiatsu foot massagers, by contrast, are typically classified as consumer wellness products.

They don’t carry the medical device designation that TENS units do — which is why they need supporting documentation to cross the IRS threshold for medical expense eligibility [3].

In practical terms: if you’re buying an EMS/TENS foot stimulator for neuropathy, you can almost certainly use your FSA or HSA card directly. If you’re buying a shiatsu massager, you’ll likely need a letter from your doctor first.

Which Foot Massagers Are FSA/HSA Eligible? (Full Breakdown)

Here’s the complete eligibility picture for every device type relevant to neuropathy:

| Device Type | Likely FSA/HSA Status | LMN Needed? | What to Know |

|---|---|---|---|

| TENS unit | Usually eligible | Usually no | TENS machines are commonly listed as eligible medical devices. |

| EMS/TENS foot stimulator | Strong eligibility case | Usually no, but plan can ask | Best when the device has clear medical-device positioning and itemized receipt language. |

| Shiatsu foot massager for neuropathy | Conditional | Recommended | Needs documentation showing it treats or manages a diagnosed condition. |

| General relaxation foot massager | Usually not eligible | May still be rejected | Fails if the primary purpose is comfort, relaxation, or general wellness. |

| Air compression leg massager | Conditional | Recommended | Stronger case when prescribed for swelling, circulation issues, or another diagnosed condition. |

| Basic foot spa / soaking basin | Usually not eligible | Not a strong claim | Generally treated as a wellness or comfort product unless a plan says otherwise. |

Plan administrators make the final decision. When a device is not clearly medical, get a Letter of Medical Necessity before buying.

| Important caveat FSA and HSA eligibility rules can vary between individual plan administrators. The table above reflects IRS guidelines and commonly accepted eligibility, but your specific plan may have additional requirements. Always confirm with your FSA/HSA administrator before purchasing — especially for items requiring a LMN. |

The Auto-Eligible Devices: No Letter of Medical Necessity Needed

These are the devices you can buy with your FSA or HSA card directly — in most cases without any additional documentation.

OSITO EMS + TENS + EPT Foot Circulation Stimulator

OSITO-style EMS/TENS foot stimulators may be a strong option for readers who want an electrical stimulation device rather than a mechanical shiatsu massager.

The FDA 510(k) record for K133929 confirms clearance for a Health Expert Electronic Stimulator, but that clearance should not be described as a cure or guaranteed treatment for diabetic neuropathy.[5]

The FDA clearance is the key differentiator — it means the device has been reviewed and classified as a medical device, not a consumer wellness product.

- 25 stimulation modes + 99 intensity levels

- 4 electrode pads for feet, calves, back, and shoulders

- 30-day trial, 3-year warranty

- Sold with FSA/HSA eligibility confirmation from manufacturer

OSITO EMS/TENS Foot Circulation Stimulator

Best fit for readers who want an electrical stimulation device rather than a relaxation-only foot massager.

- EMS/TENS-style electrical stimulation category.

- Better medical-device angle than general shiatsu massagers.

- Still confirm final eligibility with your FSA/HSA administrator.

| Full review: See our complete review of the OSITO and 9 other options in our Best Foot Massager for Neuropathy and Diabetes guide — our pillar article that covers all device types, intensity settings, and safety guidance. |

TENS Units Generally

Any standalone TENS unit marketed for pain relief is FSA/HSA auto-eligible under the same IRC 213(d)(1) classification. If you already own a TENS unit, electrode replacement pads are also typically eligible — worth noting as a recurring purchase you can run through your account.

The RENPHO and Cloud Massage shiatsu massagers both carry FSA/HSA eligibility designations from their retailers — but these are typically conditional, meaning the retailer supports FSA card payment but the underlying eligibility still depends on your plan’s documentation requirements. When in doubt, get the LMN anyway.

RENPHO Foot Massager Machine with Heat

A popular shiatsu-style foot massager for users who prefer kneading, heat, and a more traditional massage feel.

- Good option for comfort-focused foot massage.

- Some listings are marked FSA/HSA eligible.

- For neuropathy claims, a Letter of Medical Necessity is still the safer route.

Cloud Massage Shiatsu Foot & Calf Massager

Better for users who want a larger massage device that covers both feet and calves.

- Deep kneading foot and calf massage format.

- More comfort-focused than EMS/TENS devices.

- Letter of Medical Necessity is recommended for FSA/HSA claims.

Air Compression Massagers: Best With a Letter of Medical Necessity

FIT KING Air Compression Leg Massager

FIT KING fits a different user need than RENPHO or Cloud Massage. Instead of kneading the soles, it uses air compression around the calves and feet, which may be more relevant when the medical documentation mentions circulation, swelling, leg discomfort, or edema support.

- Better fit for compression-style support than deep kneading massage.

- Useful when symptoms involve calves, swelling, or circulation-related discomfort.

- FSA/HSA claim is stronger with a Letter of Medical Necessity from a doctor or podiatrist.

- Confirm your plan rules before purchase because compression devices can be handled differently by administrators.

Eligibility note: FIT KING has FSA/HSA eligible product listings on Amazon, but for neuropathy, swelling, or circulation claims, an LMN is still the safer documentation path. Retailer labeling does not override your plan administrator’s final decision.

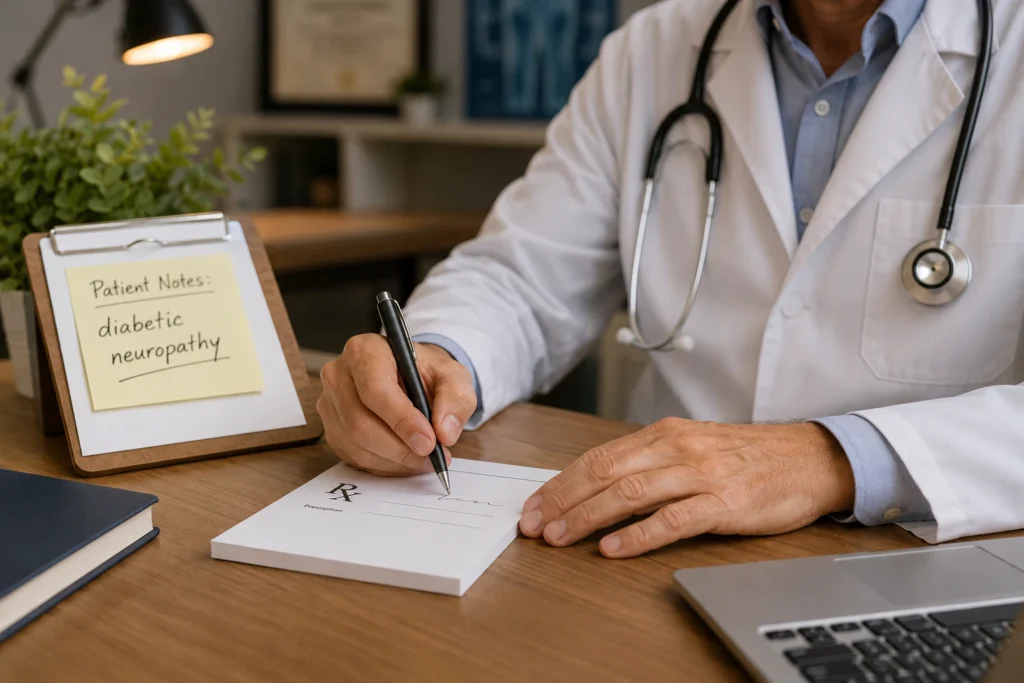

How to Get a Letter of Medical Necessity for a Foot Massager

If you’re buying a shiatsu massager and want to use FSA or HSA funds, a Letter of Medical Necessity (LMN) is what bridges the IRS gap between ‘wellness product’ and ‘medical expense.’ Here’s exactly how to get one and what it needs to contain.

Step 1: Talk to Your Doctor, Podiatrist, or Endocrinologist

Your doctor needs to confirm in writing that a foot massager is part of your treatment plan for a specific diagnosed condition — not just a recommendation for general wellbeing. For diabetics, the relevant diagnoses are typically:

- Diabetic peripheral neuropathy (ICD-10 code E11.40 or similar)

- Poor lower limb circulation / peripheral vascular disease

- Chronic foot pain associated with diabetes

- Plantar fasciitis with an underlying diabetic context

Be specific when you ask. Tell your doctor: ‘I’d like to purchase a therapeutic foot massager using my FSA funds. Can you provide a Letter of Medical Necessity explaining why this is appropriate for my neuropathy treatment?’

Step 2: The LMN Must Contain These Elements

| What a valid LMN must include Your full name and date of birth Your diagnosed condition (specific — not just ‘foot pain’) A clear statement that the foot massager is medically necessary for treating or managing this condition The specific therapeutic benefit expected (e.g. ‘improved peripheral circulation, reduction of neuropathic pain symptoms’) Expected duration of use Doctor’s name, credentials, signature, and date Doctor’s NPI (National Provider Identifier) number where possible |

Step 3: Can’t See Your Doctor Easily? Online LMN Services

Several telehealth platforms now provide LMN letters specifically for FSA/HSA purposes.

Services like Truemed and Dr. B connect you with licensed clinicians who review your health intake and issue LMNs — typically within 24 hours and for around $15–$25. This is legitimate and widely used.

That said, your own treating physician carries more weight with your FSA/HSA administrator than a telehealth service, especially if you’ve been under their care for neuropathy. Use the telehealth route when your doctor is unavailable, not as a shortcut.

How to Actually Use Your FSA or HSA to Pay for a Foot Massager

Once you have the right device and the right documentation, the process is straightforward. Here are two routes:

Route A: Pay Directly With Your FSA/HSA Card

| Direct purchase process Confirm the retailer accepts FSA/HSA cards (Amazon, Walmart, and most health retailers do) Add the device to your cart — search for ‘FSA eligible’ filter on Amazon to find auto-eligible products At checkout, select FSA/HSA card as your payment method The transaction will process automatically if the item is in the FSA-eligible product database Keep your receipt — your plan may audit purchasesIf asked for documentation later (common for larger purchases), submit your LMN |

Route B: Pay Out of Pocket, Then Submit for Reimbursement

| Reimbursement claim process Purchase the device with any payment method — keep the itemised receipt Log into your FSA or HSA account portal (online or app) Navigate to the claims or reimbursement section Upload your itemised receipt — must include: retailer name, purchase date, item description, and total cost Upload your LMN (if applicable for your device type and plan) Submit the claim — processing typically takes 5–10 business days Reimbursement is deposited back to your bank account or FSA/HSA balance |

| Year-end FSA reminder Most FSA plans require the purchase to occur within the plan year (by December 31). Some plans offer a grace period of 2.5 months or a $640 rollover allowance — check your specific plan. If you’re approaching year-end with unspent FSA dollars, buying a qualifying device before December 31 is far better than losing the money. You can verify your FSA plan details at HealthEquity, WEX, or Optum Bank — whichever administers your account. |

The Risk of Getting It Wrong: FSA/HSA Penalties

| Important — Do not misuse FSA/HSA funds If you use HSA funds for a non-qualified expense: You will owe income tax on the withdrawal amount Plus a 20% penalty tax on top — unless you are age 65 or older This applies even if the purchase was accidental or well-intentioned FSA rules are enforced differently — your plan administrator may simply reject reimbursement for non-eligible items. But incorrect use can trigger audits of your account. The safest approach: if you’re unsure whether an item qualifies, contact your plan administrator directly before purchasing. A 5-minute phone call protects you from a 20% penalty. IRS Publication 969 explains that non-qualified HSA distributions may be taxable and may also face an additional 20% tax before age 65.[3] |

FSA/HSA Eligible Foot Massagers for Neuropathy: Our Top Picks

All devices below have been reviewed in detail in our Best Foot Massager for Neuropathy and Diabetes guide. Here we summarise the FSA/HSA angle specifically.

| Device | FSA/HSA Status | Needs LMN? | Best For | Why It May Be Worth It | Amazon Link |

|---|---|---|---|---|---|

| OSITO EMS/TENS Foot Stimulator | Strongest eligibility angle | Usually not, but your plan can still ask | Electrical stimulation for neuropathy-related pain or circulation support | More medical-device aligned than general relaxation massagers. | Check on Amazon |

| RENPHO Foot Massager Machine with Heat | Conditional | Recommended | Shiatsu-style foot comfort, kneading, compression, and heat | Popular enclosed foot massager format for home use. | Check on Amazon |

| Cloud Massage Shiatsu Foot & Calf Massager | Conditional | Recommended | Foot, ankle, and calf massage coverage | Better coverage than foot-only shiatsu massagers. | Check on Amazon |

| FIT KING Air Compression Leg Massager | Conditional / stronger with documentation | Strongly recommended | Compression support, swelling, circulation-related documentation | More relevant when a clinician documents circulation, edema, or compression needs. | Check on Amazon |

Best FSA/HSA-first choice: OSITO-style EMS/TENS stimulation. Best comfort-first choice: RENPHO or Cloud Massage with a Letter of Medical Necessity. Best compression-focused choice: FIT KING with clinician documentation.

Bottom Line: Maximising Your FSA/HSA for Neuropathy Care

| Bottom Line If you have diabetic neuropathy and an FSA or HSA account, there’s a clear strategy: Buy an FDA-cleared EMS/TENS device (like the OSITO) — auto-eligible, no documentation needed, stronger eligibility case than general relaxation massagers for neuropathy pain If you prefer a shiatsu massager, get an LMN from your doctor or podiatrist first — takes one appointment and makes the purchase fully eligibleIf you have unspent FSA dollars near year-end, act before December 31 — these funds expire and cannot be recovered HSA users can take their time — funds roll over indefinitely, so you can save and spend when the right device comes along Always keep your itemised receipt and LMN together in a dedicated folder — plan administrators can ask for documentation even after a purchase is approved For the full breakdown of which foot massager is right for your specific neuropathy symptoms — not just the FSA angle — see our main guide: Best Foot Massager for Neuropathy and Diabetes. |

| Related Articles Best Foot Massager for Neuropathy and Diabetes EMS and TENS Therapy for Diabetic Neuropathy: Does It Work? |

Frequently Asked Questions

Are foot massagers FSA or HSA eligible?

It depends on the device type. TENS units and FDA-cleared EMS/TENS foot stimulators are automatically eligible under IRC 213(d)(1) — no letter of medical necessity required in most plans.

Standard shiatsu and mechanical foot massagers are conditionally eligible: they require a Letter of Medical Necessity from a licensed healthcare provider confirming medical necessity for a diagnosed condition like diabetic neuropathy.

General relaxation massagers with no medical classification are not eligible.

Do I need a Letter of Medical Necessity to buy a foot massager with FSA?

For FDA-cleared EMS/TENS devices — usually no.

For shiatsu, air compression, or other mechanical massagers — yes, in most cases.

The LMN must come from a licensed healthcare provider (doctor, podiatrist, physical therapist, or chiropractor), state your diagnosed condition, and explain why the device is part of your treatment plan.

Some plans may require it even for TENS devices on larger purchases, so confirm with your plan administrator first.

Which foot massager is the best to buy with FSA funds for neuropathy?

The OSITO EMS+TENS+EPT Foot Circulation Stimulator is the strongest choice specifically because it’s FDA-cleared as a Class II medical device, auto-eligible in virtually all FSA/HSA plans, and has the strongest peer-reviewed evidence for neuropathic pain relief.

The Cloud Massage Shiatsu is also FSA-eligible through most major retailers.

Full reviews of both are in our Best Foot Massager for Neuropathy and Diabetes guide.

What happens if I accidentally use my HSA for a non-eligible purchase?

You will owe income tax on the full amount of the non-qualified distribution, plus a 20% penalty tax on top — unless you are age 65 or older.

FSA plans typically reject non-eligible claims rather than apply penalties, but incorrect use can trigger account audits. If you’re unsure whether an item qualifies, contact your plan administrator before purchasing.

Do FSA funds expire at the end of the year?

Most do — FSA funds typically operate on a ‘use it or lose it’ basis, expiring on December 31 of the plan year.

Some plans offer a 2.5-month grace period (extending to March 15 of the following year) or allow a rollover of up to $640.

Check your specific plan documents. HSA funds never expire — they roll over indefinitely and can even be invested.

Can I use my FSA to buy replacement electrode pads for my TENS device?

Yes. Replacement electrode pads for a TENS unit are FSA and HSA eligible as consumable medical supplies, in the same way that insulin test strips are eligible.

This makes EMS/TENS devices particularly cost-effective for ongoing FSA use — the initial device and its replacement parts all qualify.

My employer’s FSA plan rejected my foot massager claim — what do I do?

First, check whether you submitted an LMN alongside the receipt. For non-auto-eligible devices, this is the most common reason for rejection.

If you submitted an LMN and were still rejected, contact your plan administrator to ask for the specific reason.

You have the right to appeal a denial — submit a formal appeal letter with your LMN, your doctor’s notes, and the IRS Publication 502 language confirming your device category’s eligibility.

Most plan administrators will approve legitimate medical device claims on appeal.

Sources & References

Sources include official IRS publications, FSA/HSA eligibility references, and FDA device records. Always confirm final eligibility with your own FSA/HSA plan administrator.

- Internal Revenue Service. Publication 502: Medical and Dental Expenses.

- FSAstore / HSAstore. TENS Machine FSA/HSA Eligibility List.

- Internal Revenue Service. Publication 969: Health Savings Accounts and Other Tax-Favored Health Plans.

- U.S. Food and Drug Administration. 510(k) Premarket Notification K133929 — Health Expert Electronic Stimulator.

- Amazon. FSA or HSA Eligible Health Products Store.

| Financial & Medical Disclaimer This article is for informational purposes only and does not constitute tax, financial, or medical advice. FSA and HSA eligibility rules are governed by IRS guidelines and individual plan administrator interpretations — always confirm your specific eligibility with your plan administrator before purchasing. |

1 thought on “FSA and HSA Eligible Foot Massagers for Neuropathy: The Complete Guide”